Tags:

Rivalry Among Existing Competitors: The Heart of Five Forces

When analyzing an industry, few factors hold as much weight as the intensity of competition between current players. This dynamic, known as rivalry among existing competitors, sits at the core of Michael Porter’s Five Forces framework. It dictates profitability, strategic direction, and long-term viability for businesses operating within a specific market sector.

Understanding this force is not merely an academic exercise; it is a practical necessity for strategic planning. High rivalry can erode margins rapidly, while low rivalry might allow for stable growth. This guide explores the mechanics of industry rivalry, the drivers behind it, and how organizations can navigate these pressures without compromising their position.

🧐 Defining Industry Rivalry

Competitive rivalry refers to the actions and counteractions taken by firms within an industry to gain an advantage over one another. It is the degree to which companies are actively competing for market share, customers, and resources. Unlike external threats like new entrants or substitutes, rivalry is internal to the industry structure.

This competition manifests in various ways:

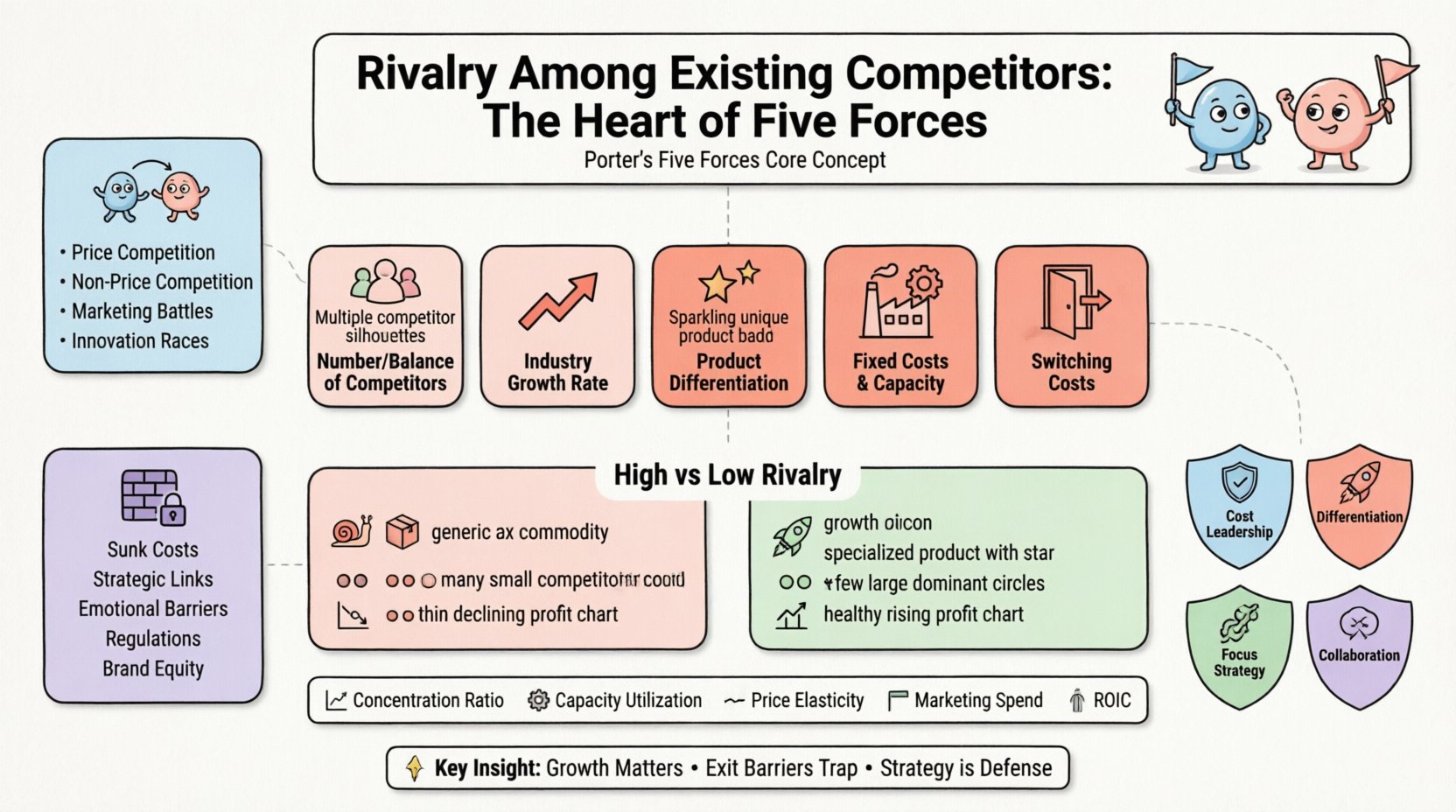

- Price Competition: Reducing prices to attract price-sensitive buyers.

- Non-Price Competition: Improving product features, service quality, or brand perception.

- Marketing Battles: Increasing advertising spend to dominate consumer attention.

- Innovation Races: Rapidly developing new technologies or processes to outpace peers.

When rivalry is intense, companies often fight over a fixed market pie. This often leads to diminished returns on investment for all participants. Conversely, when rivalry is low, firms can focus on growth and value creation rather than defensive positioning.

🚀 Core Drivers of Competitive Intensity

Several structural elements determine how fierce the competition becomes. These drivers are consistent across most industries, from manufacturing to services. Recognizing them allows analysts to predict future market behavior.

1. Number and Balance of Competitors

When an industry has many small competitors, rivalry tends to be high. No single player has the power to influence the market price or set standards. Conversely, if one or two firms dominate (a duopoly or oligopoly), they may tacitly agree to avoid destructive competition. However, if the major players are of roughly equal size, the struggle for dominance intensifies.

2. Industry Growth Rate

Growth is the great reducer of conflict. In a rapidly expanding market, companies can capture new customers without taking them from rivals. As growth slows, the market becomes a zero-sum game. Every new customer gained by one firm is a customer lost by another. This scarcity fuels aggressive tactics.

3. Product Differentiation

When products are commoditized, price becomes the primary differentiator. This leads to price wars. If a product is highly differentiated through brand loyalty, technology, or unique service, customers are less sensitive to price changes. High differentiation creates a buffer against direct rivalry.

4. Fixed Costs and Capacity

High fixed costs create pressure to fill capacity. In industries like airlines or steel manufacturing, the cost of operating a plane or a factory is high regardless of utilization. To cover these costs, firms are incentivized to lower prices to fill empty seats or idle machines, even if it means selling at a loss temporarily.

5. Switching Costs

If it is easy for a customer to switch from one provider to another, competition is fierce. High switching costs (financial, technical, or psychological) lock customers in, reducing the immediate threat of rivalry. Low switching costs empower buyers to play competitors against each other.

📊 High vs. Low Rivalry: A Structural Comparison

To better understand the impact of rivalry, it helps to contrast the characteristics of industries where competition is fierce against those where it is muted.

| Characteristic | High Rivalry Industry | Low Rivalry Industry |

|---|---|---|

| Market Growth | Slow or stagnant | High and rapid |

| Product Type | Commodity / Undifferentiated | Specialized / Differentiated |

| Exit Barriers | High (Hard to leave) | Low (Easy to exit) |

| Number of Competitors | Many equal-sized firms | Few dominant firms |

| Profit Margins | Thin and volatile | Stable and healthy |

| Strategic Focus | Cost cutting, Price wars | Innovation, Brand building |

🧱 The Critical Role of Exit Barriers

One of the most overlooked aspects of rivalry is the difficulty of leaving the industry. Exit barriers are obstacles that prevent a company from withdrawing from a market even when it is performing poorly. These barriers trap companies in a sector, forcing them to compete until they run out of resources.

Common exit barriers include:

- Sunk Costs: Investments in specialized equipment or facilities that have no resale value.

- Strategic Interrelationships: A business unit may be essential to the core brand, preventing its closure.

- Emotional Barriers: Management reluctance to admit failure or close a legacy operation.

- Government Restrictions: Regulations or labor laws that make layoffs or closures legally difficult.

- Brand Equity: The fear of damaging the overall corporate reputation by abandoning a segment.

When exit barriers are high, companies fight to the finish. They do not leave the market to reduce supply and raise prices. Instead, they remain, driving prices down further and increasing industry-wide losses. This creates a cycle of pain that can last for years.

🛡️ Strategic Approaches to Manage Rivalry

While a company cannot change the structure of its industry overnight, it can adopt strategies to mitigate the negative effects of rivalry. The goal is to carve out a protected position where the intensity of competition matters less.

Cost Leadership

Becoming the lowest-cost producer allows a firm to compete on price while maintaining margins. If the industry is price-sensitive, the cost leader can withstand price wars longer than competitors. This requires rigorous efficiency and scale.

Differentiation

Creating a product or service that is perceived as unique reduces the direct comparison with competitors. Customers pay a premium for the perceived value, making them less likely to switch based on a minor price change. This could involve superior customer service, proprietary technology, or a strong brand narrative.

Focus Strategy

Targeting a specific niche allows a firm to serve a particular segment better than broad competitors. By dominating a small slice of the market, the company avoids head-on collisions with larger players. This works well when the niche has specific needs that generalists ignore.

Collaboration and Alliances

In some cases, competitors may collaborate on industry-wide issues, such as setting safety standards or lobbying for favorable regulations. While price-fixing is illegal, cooperation on non-pricing issues can stabilize the market environment.

🔗 Interplay with Other Competitive Forces

Rivalry does not exist in a vacuum. It interacts dynamically with the other four forces of the framework. Understanding these connections provides a holistic view of the competitive landscape.

Impact on Supplier Power

When rivalry among competitors is high, the industry’s overall profitability drops. This weakens the bargaining power of suppliers. If the industry is fighting for survival, suppliers cannot demand higher prices because the buyers have no margin to spare. Conversely, if the industry is highly profitable due to low rivalry, suppliers have more leverage.

Impact on Buyer Power

High rivalry often benefits buyers. When competitors fight for market share, they offer better terms, discounts, and services to customers. This increases buyer power. If rivalry is low, buyers have fewer options and less leverage, forcing them to accept standard terms.

Impact of Substitutes

The threat of substitutes limits the price a company can charge. If rivalry is high, companies cannot raise prices to fund innovation because customers will switch to substitutes. If substitutes are weak, companies can use the profits from low rivalry to invest in defending against future threats.

📈 Metrics for Assessing Competitive Pressure

To move from qualitative analysis to quantitative measurement, several metrics can help assess the level of rivalry in a specific sector.

- Concentration Ratios: The percentage of market share held by the top four or eight firms (CR4 or CR8). Low concentration usually implies higher rivalry.

- Capacity Utilization Rates: If utilization is consistently low, firms are likely overbuilding and competing aggressively for volume.

- Price Elasticity: If small price changes lead to large volume changes, competition is likely intense.

- Marketing Spend as % of Revenue: High advertising spend relative to revenue often indicates a battle for attention and share.

- Return on Invested Capital (ROIC): Consistently low ROIC across the industry suggests that rivalry is consuming profits.

🌍 Real-World Contexts

Consider the airline industry. It is characterized by high fixed costs, commoditized products (a seat is a seat), and low switching costs. This results in intense rivalry. Margins are thin, and companies constantly battle for loyalty programs and route dominance.

Contrast this with a specialized medical device manufacturer. They face high barriers to entry due to regulation and patents. Products are highly differentiated. Rivalry exists but is focused on innovation and clinical trials rather than price. The structure protects margins.

Another example is the retail sector. Traditional brick-and-mortar stores face immense rivalry from e-commerce giants. The barrier to entry for online retail is lower, leading to a surge in competitors and aggressive pricing strategies. Physical retailers must now differentiate through experience to survive.

🧭 Navigating the Future

Competitive landscapes are not static. Technology, regulation, and consumer behavior shift the balance of rivalry over time. A market that is calm today may become a battlefield tomorrow. For instance, the rise of digital platforms has disrupted traditional retail, increasing rivalry in ways that were previously impossible.

Strategic agility is key. Organizations must continuously monitor the drivers of rivalry. If growth slows, they must prepare for a more aggressive competitive environment. If new entrants appear, they must assess whether the market is becoming saturated.

Effective management of rivalry requires a clear understanding of the industry structure. It demands discipline to avoid reactive price cuts and the creativity to find differentiation. By focusing on long-term value creation rather than short-term tactical wins, companies can endure periods of high competition.

📝 Summary of Key Insights

- Intensity Varies: Rivalry ranges from mild to aggressive based on industry structure.

- Growth Matters: Slow growth typically triggers fiercer competition for share.

- Exit Barriers Trap: High barriers prevent weak firms from leaving, prolonging industry pain.

- Strategy is Defense: Cost leadership and differentiation are primary shields against rivalry.

- Metrics Guide: Use concentration ratios and utilization rates to measure pressure.

By mastering the dynamics of rivalry, businesses can make informed decisions about where to play and how to win. It remains the central force in determining the economic profitability of an industry.

Comments (0)